This is the first article in a series covering basic concepts related to money. I first created this content as a presentation for my kids when they were in college to introduce them to important concepts around money and finances. I wanted to give them an overview of how money works in the “real” world so that when they started working full-time, they would be better informed and prepared on how to manage money responsibly. I’ve since adapted it into a set of short articles for anyone who wants a clearer understanding of how money really works — and how to manage it wisely.

Why is This Important?

While most of the information presented here might be considered common knowledge, the fact is that most of these topics are not covered in any sort of educational curriculum - at least not in my kids’ cases - so I wanted to capture what I felt were the essentials and pass them on to my children.

“Money can’t buy happiness, but neither can poverty.”

Money isn’t everything, but the truth is, we live in a world where money is important. Money can provide the means and freedom to make decisions in life, be it in the small, such as where you want to eat, or for things more significant, like where you want to vacation, whether you want to leave your job, or where you want to ultimately live.

As we’ll see, money has a compounding effect that can work for you if you form good habits early — or against you if you don’t.

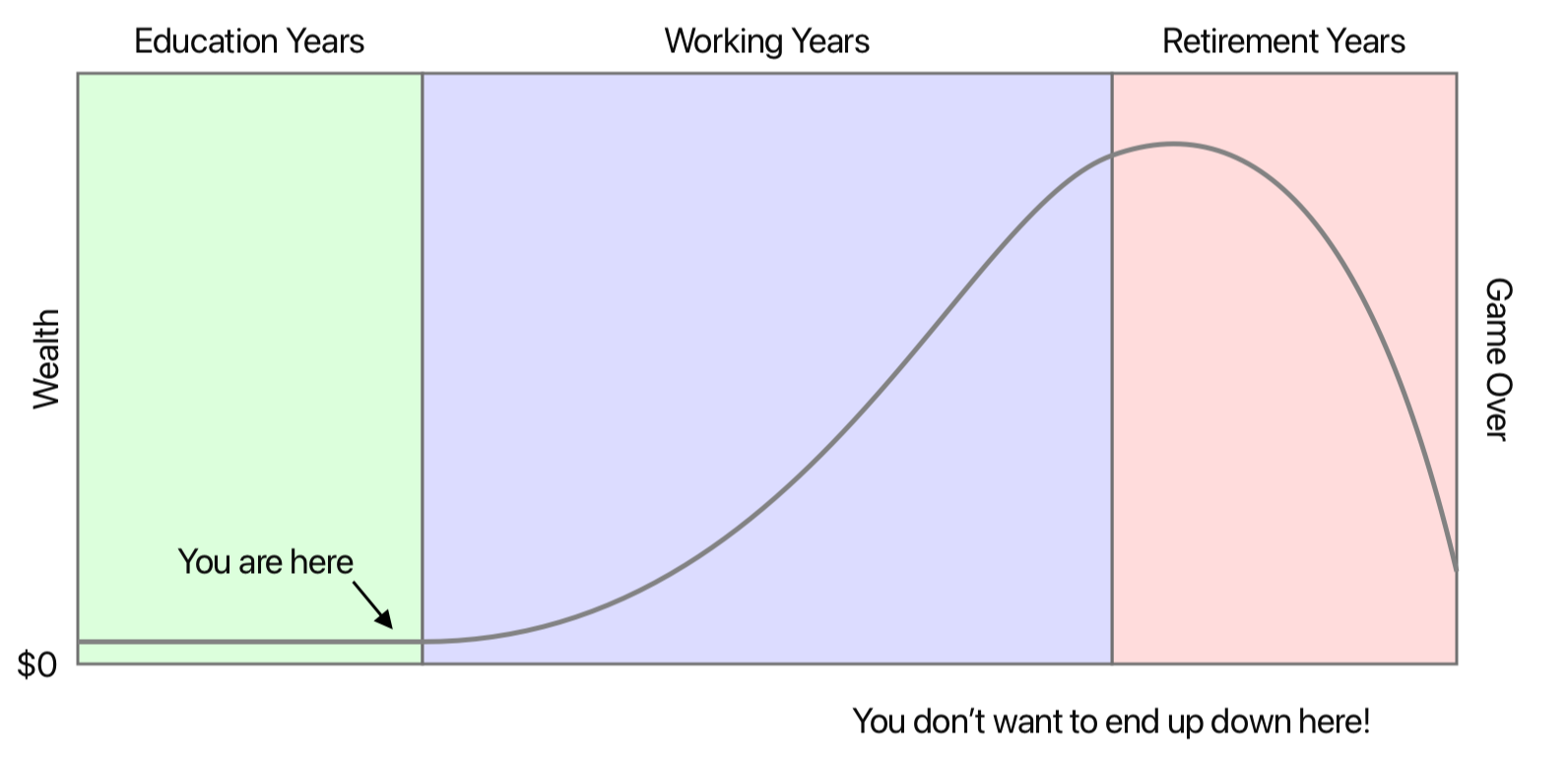

Life’s Three Phases:

Learn, Earn, and Burn

A simplistic, but useful way to think of your life is breaking it into three general phases that cover learning through your school years, earning a living through your career, and then spending your retirement savings once you stop working, which I call “learn, earn and burn”.

The three phases of your financial life

The three phases of your financial life

If you consider that most people live to be 80 or 90, then you will spend roughly the first quarter of your life learning, graduating high school in your late teens, or graduating college in your early 20s.

Then you’ll spend the next half of your life, say 40-45 years, working and earning money. Hopefully, you’ll find something that you enjoy doing and are also good at, enabling you to build a successful career over that period.

The last quarter of your life will likely be spent in retirement, living off the money you accumulated over those earning years. It’s in this last phase that you’ll “burn” through your retirement savings doing things like traveling and hopefully enjoying life with all the free time you’ll have in this later stage. This specific path of life isn’t a rule, of course, but the majority of people experience some variation on this theme.

Many Questions to Answer

Throughout adulthood, you’ll encounter countless financial questions — some big, some small:

- What happens to your income?

- What are all those deductions on my paycheck?

- How much of your paycheck should you save?

- Should I follow a budget? It sounds like a pain.

- How is a credit card different than a debit card?

- What should you do with your savings?

- What is a 401k plan? An IRA?

- What does “leasing” a car mean?

- What are stocks? Bonds? ETFs?

- What’s a mortgage? (and why don’t they just call it a loan?)

- How does insurance work? Do I need it?

At first, you may think these questions aren’t important and that understanding how some of these things work isn’t useful information. But before you know it you’ll be facing important financial decisions that can have a big impact on your life.

- You’ll be asked to make some decisions at your job about contributing some of your money to a savings plan or health savings account. You will also likely be asked to choose a health insurance plan.

- Your savings plan will require you to make investment elections to determine how that money is actually invested

- You will need to choose where to live and how much you should spend on rent

- You’ll be offered all kinds of deals to sign up for credit cards that seem easy to get and convenient to have

- Later in life, if you need a car, you’ll need to decide if you want to buy it or lease it. If you buy it, you will probably need a loan. You’ll also need to get auto insurance before you can buy the car.

- When you get to the point of buying a home someday, you’ll also need a special loan called a mortgage, and you’ll also need more kinds of insurance for your home.

These are some of the questions we’ll address in these posts, along with lots of other important topics around money.

“An investment in knowledge pays the best interest.”

Financial literacy doesn’t just help you avoid mistakes — it gives you options. It allows you to be in control of your financial life instead of it controlling you.

A Tour of What’s Ahead

Before diving in, here is a list of topics covered in this series.

- Money management, touching on banking, income, expenses, and budgeting

- Saving and investing concepts to help you grow the money you save along the way

- Loans and mortgages and the responsible use of debt as well as the risks of getting into too much debt

- Credit - how to build your credit history, what a credit score is, and why it’s important

- How insurance works, the many forms of insurance, and how it can be used to protect against financial risks

- A deeper dive into investing to learn more details, including risk and diversification, before we touch on a few of life’s big financial decisions

Along the way, we’ll highlight key financial ideas, or “key concepts”, that will help you interpret the financial world around you and make smarter choices.